If you're considering buying an NS&I Savings Certificate, especially the (RPI-) index-linked version, you may need to decide quickly.

NS&I's site says they "expect [them] to be on sale for a sustained period of time", which gives them room for manoeuvre as to timing and could leave ditherers suddenly high and dry. They also say "we are currently experiencing high volumes of calls" and this could mean that they will reach their overall sales target well before the end of the financial year - which is why, reportedly, the Certificates were withdrawn from sale last July . It's also worth noting that there is no specific target for Savings Certificates - as I reported here last month, it is merely expected that NS&I will end the tax year managing £2 billion more than it did at the beginning - spread over all its products, including e.g. Premium Bonds.

Moreover, there is commercial pressure to withdraw the Certificates. I reported that they were back on 12 May, and a mere two weeks later the Nationwide Building Society began complaining of "unfair competition" from NS&I.

The Government is in a cleft stick: people should have a secure and inflation-proof haven for their cash, but it is also a priority to get banks and building societies lending again to stimulate the economy.

It has also been observed that since the financial sector has been allowed to dominate the economy, the Treasury has become semi-dependent on taxes on bankers' bonuses. I have to bite my tongue at this point!

Actually, the competition complained of is not as fearsome as it was. True, you can invest up to £15,000 for a 5-year period (and can also buy them for children aged seven or more); but the 2- and 3- year versions are no longer available for new purchases (existing ones can usually be rolled-over on maturity), so the maximum you can invest has been sharply reduced: in 2006 you could have committed up to £45,000 per person, by buying three different versions at the same time!

Further, although the Certificates are still RPI-linked and tax-free, the additional interest is now only 0.5% per year. As before, you can access the cash before the end of the 5-year term (I suspect this term was chosen as being the least attractive), but you lose a year's interest.

Having said that, I still think they are better than what you can get elsewhere. As this FT article says (see end), the commercial alternatives are either taxable or carry a degree of investment risk.

If you do want to get in (and remember, this is NOT a personalised recommendation!), do so before the market whinges the Government into submission. You can apply online here.

INVESTMENT DISCLOSURE: We're just considering buying some ourselves!

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Saturday, 28 May 2011

Thursday, 12 May 2011

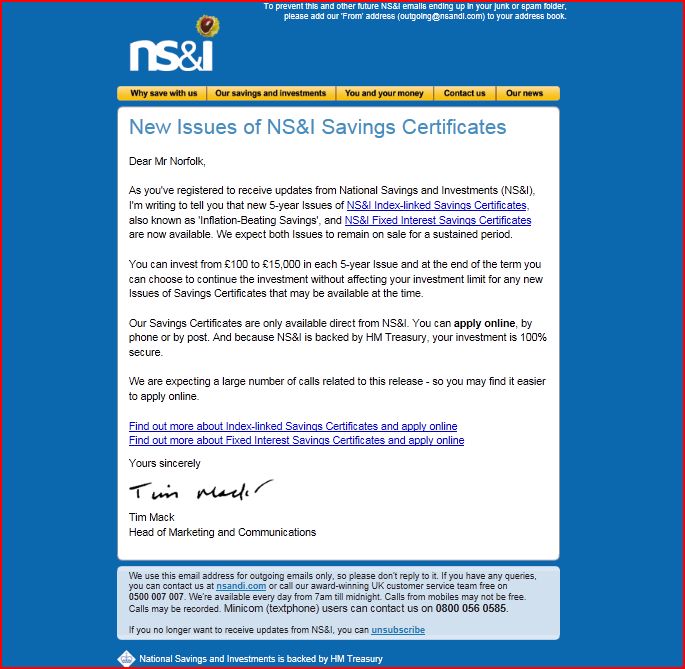

NS&I Savings Certificates return!

Five-year index-linked and fixed rate NS&I Certificates are now available again, according to a hotline email received here today.

Demand is likely to be high so if you want to get in, NS&I recommend applying online.

INVESTMENT DISCLOSURE: None. Still in cash, and missing all those day-trading opportunities.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Demand is likely to be high so if you want to get in, NS&I recommend applying online.

INVESTMENT DISCLOSURE: None. Still in cash, and missing all those day-trading opportunities.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Tuesday, 3 May 2011

Credit cards and consumer protection

As reported in the Daily Mail today, you get additional consumer protection if you make a purchase of an item worth £100 or more by using your credit card.

The Mail piece is based on details on page 16 in the latest issue of "Ombudsman News", a regular publication by the Financial Ombudsman Service (aka FOS -see link in sidebar under "Financial Regulators (UK)"). In the case cited, a student had bought what turned out to be a faulty computer and when she complained, the shop advised her to contact the manufacturer; but she didn't have time to do this, so she sought redress from the credit card issuer instead. When the issuer refused, the FOS ruled in the student's favour.

Section 75 of the Consumer Credit Act 1974 (current version) states:

"If the debtor under a debtor-creditor-supplier agreement falling within section 12(b) or (c) has, in relation to a transaction financed by the agreement, any claim against the supplier in respect of a misrepresentation or breach of contract, he shall have a like claim against the creditor, who, with the supplier, shall accordingly be jointly and severally liable to the debtor."

"Jointly and severally" means that the consumer does not have to deal with the shop or the manufacturer first, he/she can get the money back from the credit card company; but the supplier can also be dragged into the action, if the consumer so chooses.

This does not apply if the purchase is via a "non-commercial agreement", or if the item cost less than £100 or more than £30,000, or if the credit card terms have been breached (e.g. by exceeding the credit limit on the account).

In the definitions section of the Act, "“non-commercial agreement ” means a consumer credit agreement or a consumer hire agreement not made by the creditor or owner in the course of a business carried on by him" - in other words, loosely speaking, the transaction has to have been commercial rather than private.

Worth buying a car from a dealer this way, perhaps?

INVESTMENT DISCLOSURE: None. Still in cash, and missing all those day-trading opportunities.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

The Mail piece is based on details on page 16 in the latest issue of "Ombudsman News", a regular publication by the Financial Ombudsman Service (aka FOS -see link in sidebar under "Financial Regulators (UK)"). In the case cited, a student had bought what turned out to be a faulty computer and when she complained, the shop advised her to contact the manufacturer; but she didn't have time to do this, so she sought redress from the credit card issuer instead. When the issuer refused, the FOS ruled in the student's favour.

Section 75 of the Consumer Credit Act 1974 (current version) states:

"If the debtor under a debtor-creditor-supplier agreement falling within section 12(b) or (c) has, in relation to a transaction financed by the agreement, any claim against the supplier in respect of a misrepresentation or breach of contract, he shall have a like claim against the creditor, who, with the supplier, shall accordingly be jointly and severally liable to the debtor."

"Jointly and severally" means that the consumer does not have to deal with the shop or the manufacturer first, he/she can get the money back from the credit card company; but the supplier can also be dragged into the action, if the consumer so chooses.

This does not apply if the purchase is via a "non-commercial agreement", or if the item cost less than £100 or more than £30,000, or if the credit card terms have been breached (e.g. by exceeding the credit limit on the account).

In the definitions section of the Act, "“non-commercial agreement ” means a consumer credit agreement or a consumer hire agreement not made by the creditor or owner in the course of a business carried on by him" - in other words, loosely speaking, the transaction has to have been commercial rather than private.

Worth buying a car from a dealer this way, perhaps?

INVESTMENT DISCLOSURE: None. Still in cash, and missing all those day-trading opportunities.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Monday, 2 May 2011

A letter to Douglas Carswell MP

Monday, 02 May 2011

Douglas Carswell MP

The House of Commons

London

SW1A 0AA

Dear Sir

Financial Services (Regulation of Deposits and Lending) Bill 2010-11

Congratulations on your speech introducing the above Bill, which I have just seen on YouTube. May I offer some counter-arguments so that you can rebut them when others raise them?

• Were your Bill to become law, the banks might simply offer no interest on “storage bank accounts” and a sufficient differential on “investment accounts” to draw money away from the former, even from cautious savers (but still not enough in the latter case to match inflation). In fact something like this is already happening with people investing in stocks who shouldn’t.

• British business might be at a disadvantage if we have this rule but other countries don’t. Look what the US has already bought from us with “candyfloss money” – the old Cadbury Quakers must be spinning in their graves.

• Savings need to be safe in terms not only of the return of capital, but the return of its real value. NS&I Index-Linked Savings Certificates fitted that bill, and were withdrawn in 2010 for the first time in 35 years. This is an indication of the Government’s priorities, surely. But even when available, money had to be locked up in those Certificates for years. And when first introduced, they were only available to pensioners.

• If you really want sound money for the protection of ordinary savers, then we should have index-linked (and linked to a properly fair index of consumer price inflation), instant-access (or short-notice access) cash ISAs, so that deferred consumption is at least not penalised, if not positively rewarded.

Very best wishes to you and for your Bill,

Rolf Norfolk

INVESTMENT DISCLOSURE: None. Still in cash, and missing all those day-trading opportunities.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Douglas Carswell MP

The House of Commons

London

SW1A 0AA

Dear Sir

Financial Services (Regulation of Deposits and Lending) Bill 2010-11

Congratulations on your speech introducing the above Bill, which I have just seen on YouTube. May I offer some counter-arguments so that you can rebut them when others raise them?

• Were your Bill to become law, the banks might simply offer no interest on “storage bank accounts” and a sufficient differential on “investment accounts” to draw money away from the former, even from cautious savers (but still not enough in the latter case to match inflation). In fact something like this is already happening with people investing in stocks who shouldn’t.

• British business might be at a disadvantage if we have this rule but other countries don’t. Look what the US has already bought from us with “candyfloss money” – the old Cadbury Quakers must be spinning in their graves.

• Savings need to be safe in terms not only of the return of capital, but the return of its real value. NS&I Index-Linked Savings Certificates fitted that bill, and were withdrawn in 2010 for the first time in 35 years. This is an indication of the Government’s priorities, surely. But even when available, money had to be locked up in those Certificates for years. And when first introduced, they were only available to pensioners.

• If you really want sound money for the protection of ordinary savers, then we should have index-linked (and linked to a properly fair index of consumer price inflation), instant-access (or short-notice access) cash ISAs, so that deferred consumption is at least not penalised, if not positively rewarded.

Very best wishes to you and for your Bill,

Rolf Norfolk

INVESTMENT DISCLOSURE: None. Still in cash, and missing all those day-trading opportunities.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Subscribe to:

Posts (Atom)